|

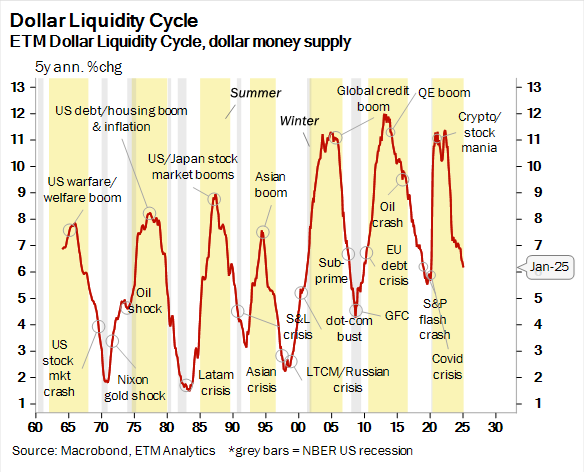

Liquidity Tightening and the Federal Reserve Outlook Liquidity conditions in the U.S. financial system continued to tighten through January and February 2025, with all indicators suggesting that this trend has persisted into March. A key indicator underscoring this development is the significant drop in reverse repo transactions accepted by banks, signaling a near absence of excess liquidity in the banking system.

Data from the Federal Reserve Bank of New York shows that current reverse repo levels are approaching pre-pandemic norms, reflecting a return to more restrictive monetary conditions. As quantitative tightening (QT) remains in force, speculation is mounting that ending QT may emerge as a central theme for 2025. Consequently, markets are increasingly anticipating that the Federal Reserve may implement up to three rate cuts of 25 basis points each before year-end. |

|

|

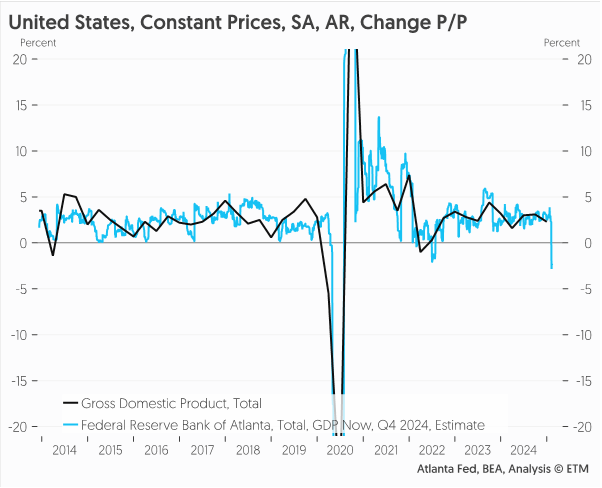

Sharp GDP Downgrade Raises Recession Fears The GDP Now tracker delivered a surprise to market watchers, plummeting from 3.9% growth expectations to -2.8% in just four weeks. This sharp contraction has fueled concerns about a potential U.S. recession.

A deeper dive into the data reveals that net exports were the primary drag on GDP, as U.S. companies rushed to import production inputs ahead of anticipated Trump-era tariffs. Although trade flows might normalize post-tariff implementation, price impacts from duties and potential counter-tariffs may cap any rebound. This trend offers investors early insight into how disruptive tariffs could be to U.S. economic performance. |

|

|

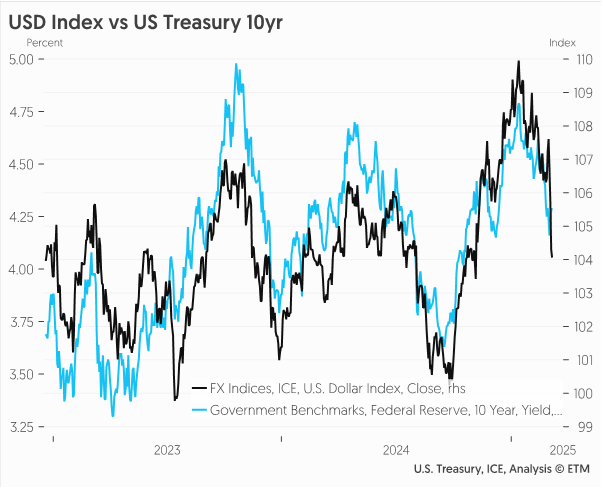

Bond Yields, USD Weakness, and Emerging Markets Impact Historically, there has been a strong correlation between U.S. bond yields and the trade-weighted U.S. dollar (USD). As yields decline, the USD typically weakens, and that pattern is holding true as markets adjust to worsening growth prospects and possible Fed rate cuts.

In response, Fed funds futures now reflect expectations for a more accommodative stance, pricing in three separate 25 basis point cuts by the end of 2025. This shift implies that U.S. exceptionalism—marked by higher yields and robust growth—may erode, potentially putting the USD under pressure.

While a weaker USD could benefit emerging market currencies like the Rand, the caveat is that rising global risk aversion, driven by falling equity markets or geopolitical tensions, could curb this potential upside. The VIX volatility index remains a critical barometer of such risks, especially given the correlation between emerging markets debt and equity performance. |

|

|

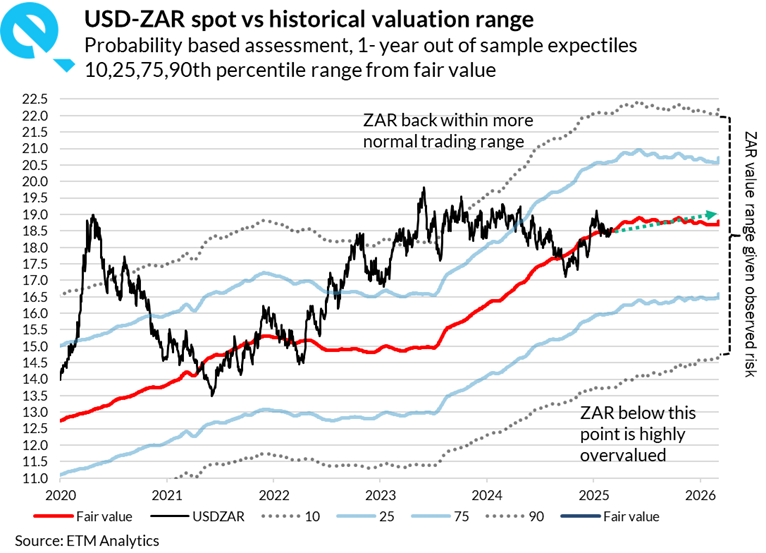

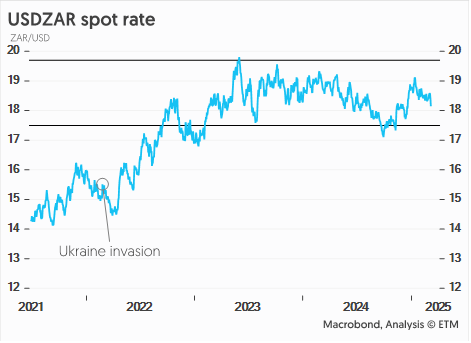

Rand Holds Steady Amid Global Uncertainty, Supported by Strong Trade and Fed Rate Cut Expectations The Rand remains close to its risk-adjusted fair value against the U.S. dollar, showing resilience despite domestic and global uncertainties. Supported by strong terms of trade, particularly rising gold and commodity prices, and expectations of continued trade surpluses, the rand has been buoyed by favourable external factors, including a weaker USD as markets price in up to three Fed rate cuts in 2025.

Although the SARB is expected to cut rates once more this year, caution prevails amid volatile global markets and fiscal risks tied to South Africa’s upcoming budget. Against other major currencies, the rand shows mixed signals: marginal overvaluation against the euro, a slight undervaluation against the pound due to pending fiscal risks in both countries, and overvaluation versus the Australian dollar driven by diverging monetary policy outlooks.

Overall, while some near-term volatility is possible, sustained supportive factors suggest any ZAR depreciation will likely be limited and short-lived. We believe the rand will trade in a broader R18.00 to R19.00 range, with the rand closer to the R18.00 level at year end. |

|

|

|

Policy Risks and Global Market Sentiment U.S. policy decisions, particularly around tariffs and potential government layoffs, represent significant threats to economic stability and global investor confidence. Tariffs could undermine U.S. GDP growth and stifle corporate earnings, while political dysfunction may erode economic dynamism. A sustained downturn in S&P 500 performance could weigh heavily on emerging market assets, despite broader USD trends.

Conclusion As we head deeper into 2025, liquidity tightening, recession risks, tariff impacts, and monetary policy shifts will dominate financial markets. Investors must navigate a landscape marked by uncertainty around U.S. economic resilience and its global repercussions—particularly for emerging markets like South Africa. Keeping a close watch on the Fed’s response to deteriorating growth metrics and geopolitical developments will be key to managing risks and seizing opportunities. |