|

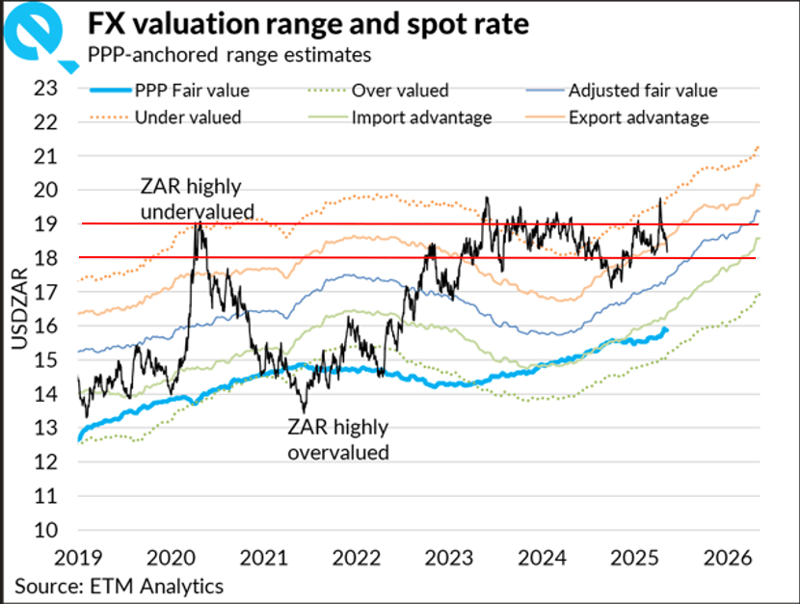

Currency: The Rand has strengthened recently as global trade tensions ease and concerns around South Africa’s Government of National Unity (GNU) have calmed. While uncertainty and market volatility remain, especially for riskier assets like the ZAR, there’s cautious optimism that a reform-focused budget and supportive global conditions, like potential U.S. interest rate cuts, could help the rand appreciate further. However, at current levels near R18.20/USD, the currency doesn’t offer a substantial advantage for either exporters or importers. The ZAR is still in the R18.00 to R19.00 range for the foreseeable future. |

|

|

Inflation: Headline CPI inflation slowed to +2.7% y/y in March from February’s +3.2% y/y. Core CPI (excl. volatile food and energy prices) slowed to +3.1% y/y in March, from 3.4% y/y in February. Inflation is now lower than the lower band of the SARB’s 3%-6% inflation target. Inflation is anticipated to decrease further next month, mainly due to even lower fuel prices. The VAT hike has now been scrapped, which limits upside risks to inflation. Repo rate: The SARB kept the repo rate at 7.50% in March after three consecutive 25bp cuts. The bank took a cautious approach despite inflation being within the target range, with domestic and global uncertainties influencing the decision. While much will depend on the extent of US Fed rate cuts, we expect only one more rate cut this year. The SARB could pause its rate-cutting cycle in May as it awaits more clarity on US President Trump’s tariff pause. Government Finances: From a year-to-date perspective, the budget deficit stood at -R323bn in February, broadly in line with the -R326bn in the corresponding period last year, even though the majority of GFECRA funds were allocated last year to reduce existing debt. The government’s fiscal position remains challenging, with a debt-to-GDP at roughly 75%. Austerity measures need to be implemented. The tabling of a new Budget on May 21 is a key event to determine the appetite for the government to undertake reforms following the recent disagreement between the ANC and the DA on the now-scrapped budget. GDP Growth: SA’s GDP expanded by 0.6% q/q in Q4 from -0.3% q/q in Q3. On a year-on-year basis, GDP growth came in at 0.9% y/y in Q4, up from Q3’s 0.3% y/y. Agriculture saw the most significant rebound, expanding by 17.2% after a sharp -28.8% decline in Q3, driven primarily by increased economic activity in field crops and animal products. This slight uptick will likely continue into 2025. However, economic growth will likely fall short of the government’s 3% target, which requires foreign investment to revitalise the nation’s neglected infrastructure. Offshore conditions: While there has been some recovery in markets since Trump announced a complete three-month pause on all the “reciprocal” tariffs on April 9, uncertainty and volatility remain the order of the day. While there is no sign of the trade war between the US and China abating, there appears to be some progress on trade relations with other countries; US officials are not yet naming the countries involved. Nonetheless, Trump continues to double down on his aggressive tariff stance and has taken aim at US Fed Chair Jerome Powell on more than one occasion, asserting that he has a better understanding of interest rates than Powell. Such comments cause jitters in the market. The US Fed has the task of choosing between fighting tariff-driven inflation or a growth slump, with the Fed funds futures pricing in 3 rate cuts by the end of the year and an 80% chance of a fourth cut. |