|

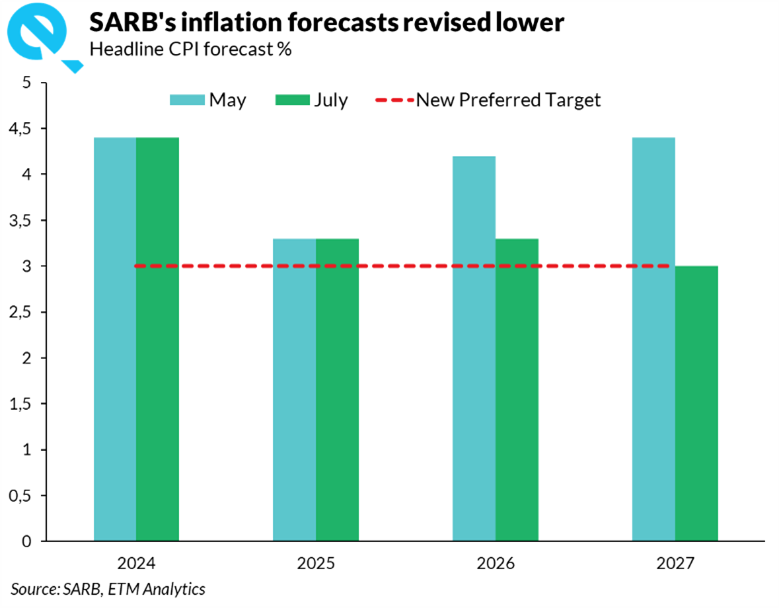

The SARB cut its benchmark rate by 25bp to 7.00%, matching consensus estimates and our base case. This wasn’t surprising given the benign inflation environment that SA currently enjoys. Consumer inflation is still near multi-year lows, while inflation expectations have moderated notably. Note that the SARB’s inflation forecasts were lowered over the next two years, with inflation expected to average 3.3% this year and in 2026, with the prior forecasts pegging headline inflation at 4.2% y/y for 2026. The estimate for 2027 was similarly lowered to 3.0% from the 4.7% expected at the prior MPC meeting. Economic growth metrics, however, remain weak and barring the absence of some significant structural reforms, the outlook for GDP growth remains subdued. The SARB’s own leading indicator dropped 1.3% m/m to 111.3 points in May, down from a revised 112.7 in the month prior, marking the third straight decline since March. While still close to November’s 114.7 peak, its highest since late 2022, the drop reflects weakening momentum. ETM’s proprietary indicators also favour lower interest rates going forward, with inflation risk declining notably from earlier this year, while our ZAR sentiment indicator remains firmly bullish on the local currency. This implies that, in the absence of another negative stressor, the ZAR should appreciate from current levels, particularly in the event of USD weakness, as the Fed is still expected to cut rates later this year. Overall, the meeting was a fairly dovish one and raised expectations within financial markets that further rate cuts are coming, a view supported by the downward revisions to the SARB’s QPM. However, one must remain aware of the risks ahead, given that South Africa still does not have a new trade deal with the US and finds itself in the crosshairs of Trump and several other prominent lawmakers. Furthermore, anchoring inflation at the new 3% target (whether it is official or not) will be difficult if interest rates are cut further. |

|

Analysis |

|

|

Perhaps the most notable piece of information from the July MPC meeting was that the SARB is now looking to anchor inflation at 3%, the lower bound of its current target range. This is not an official change to the target but a shift in the SARB’s thinking and perhaps an implicit message that the official change to a set 3% inflation target is coming. The forecasts presented were estimated using the new 3% target, aimed at highlighting the macroeconomic benefits of lower inflation over the long term. As we have noted before, now is the opportune time to change the central bank’s mandate, as it would be much more difficult to rein in higher inflation than to keep already subdued inflation stable, especially in an environment of only moderate economic growth. |